Stablecoins and tokenization in 2026: is crypto becoming financial infrastructure?

For years, the crypto market was viewed primarily as a space for speculation, cyclical waves of optimism, and periodic regulatory shocks. Yet in 2026, it is becoming increasingly difficult to ignore the fact that beneath that visible, volatile layer, something far more serious is taking shape: a parallel financial infrastructure built on blockchain networks.

At its center are no longer just Bitcoin and altcoins, but stablecoins, tokenized treasury products, on-chain funds, and the first serious attempts to move traditional financial assets into a programmable digital form. In other words, the focus is slowly shifting from the question of “which token will rise” to “which parts of the financial system can operate more efficiently on-chain.”

That does not mean the transition is complete. On the contrary, the current phase looks more like an early infrastructure layer than a mature new system. Stablecoins have already reached massive scale, while the rest of tokenized assets remains relatively small compared with traditional markets. Still, the gap between those two categories is exactly what explains where the market stands today.

That is why it is important to distinguish between two parallel processes. The first is the expansion of stablecoins as a digital form of dollars and liquidity. The second is the slower, but strategically far more important, growth of tokenized real-world assets — from treasuries to stocks and funds. Only when these two processes are viewed together does it become clear that crypto is no longer just a market for trading, but a candidate for a new base layer of financial infrastructure.

Executive Summary

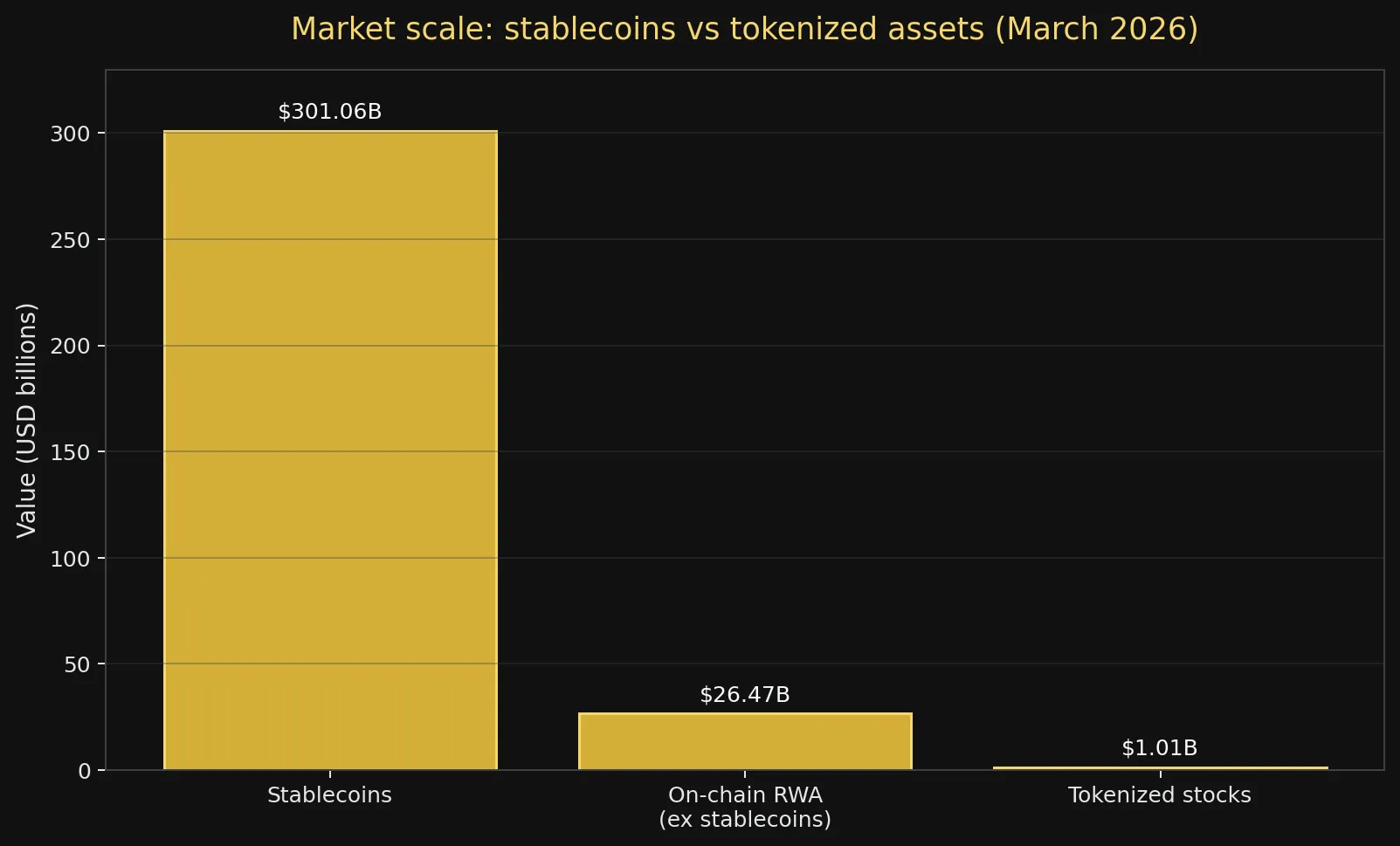

- In March 2026, stablecoins reached roughly $301 billion in market value, making them many times larger than the rest of on-chain tokenized assets.

- The on-chain RWA market excluding stablecoins stands at around $26.47 billion, showing that tokenization is still in an early but rapidly expanding institutional phase.

- Tokenized stocks have surpassed $1 billion, still a small segment, but a symbolically important step toward an on-chain version of traditional capital markets.

- The European regulatory view is becoming more cautious because of the potential outflow of bank deposits, while the US approach currently leans toward more technology-neutral treatment.

- The key implication is not that blockchain will “replace finance,” but that part of financial infrastructure could become programmable, more accessible, and operationally more efficient.

Illustration: Stablecoins now carry the largest share of on-chain liquidity, while tokenized assets are gradually building a new financial infrastructure.

1. Context and market background

After several years in which the dominant narrative was shaped by market crashes, platform collapses, and regulatory uncertainty, 2026 brings a visible shift. The most important development is no longer just the price of crypto assets, but the growth of infrastructure that enables the transfer, storage, and settlement of value on blockchain networks.

Stablecoins are the first segment to reach serious operational scale. Their function is simple, but highly powerful: they enable a digital dollar that can be transferred 24/7, used in trading, payments, international transfers, and various on-chain services. That is exactly why stablecoins now represent the clearest example of blockchain moving from the speculative zone into infrastructure.

The second wave is tokenization of real-world assets. This category includes tokenized treasuries, private credit, funds, commodities, and even publicly listed stocks in tokenized or synthetic form. Unlike stablecoins, which already have broad usage, tokenization of other asset classes is still in the market-building phase. Even so, its strategic relevance is substantial because it opens the door to markets that could operate with lower settlement costs, greater programmability, and broader global access.

That is why 2026 does not look like a year in which “crypto is rising again,” but rather a year in which infrastructure is becoming more clearly separated from speculation. The process is slower than optimists expected in 2021 or 2022, but it is now far more serious because it is being driven by data, institutional products, and regulatory signals.

2. Data and numerical analysis

The simplest way to understand the current state of the market is to compare the scale of stablecoins with the rest of tokenized assets.

According to current data from RWA.xyz, the total value of stablecoins stands at around $301.06 billion. At the same time, the total on-chain value of tokenized real-world assets excluding stablecoins is about $26.47 billion, while tokenized stocks have reached approximately $1.01 billion. This gap shows that digital money is far ahead of digitized assets. Stablecoins are already liquidity infrastructure; tokenization of other asset classes is still trying to reach a similar level of network effect.

| Segment | Value | Comment |

|---|---|---|

| Stablecoins | $301.06B | Already functioning as a digital liquidity base |

| On-chain RWA (ex stablecoins) | $26.47B | Early but rapidly growing phase of tokenization |

| Tokenized stocks | $1.01B | A small segment, but an important sign of market expansion |

| Tokenization projection by 2030 | ~$2T | McKinsey base-case scenario, excluding crypto and stablecoins |

These figures reveal several important points.

First, stablecoins have already moved beyond the experimental stage. Once a market reaches hundreds of billions of dollars, it is no longer just a niche innovation. It is a signal that there is durable demand for a digital dollar that moves faster and more flexibly than traditional banking channels.

Second, tokenization of real-world assets is much smaller, but that does not make it irrelevant. On the contrary, its relatively small absolute size compared with stablecoins shows that we are still in the early stage of a potentially much larger transformation. In infrastructure transitions, the first phase is often not dominance in scale, but validation of the model.

Third, the tokenized stocks and funds segment suggests that the market is no longer limited to bonds and treasury products. Even if it remains small, this part of the market shows that the logic of tokenization is expanding toward instruments traditionally handled by brokers, exchanges, and central depositories.

That is why the most important question may not be how large tokenization is today, but whether it has become large enough to be strategically relevant for banks, funds, and regulators. More and more signals suggest that the answer is yes.

3. Visual analysis (Chart)

A comparison of current market scale clearly shows that stablecoins represent the central infrastructure layer of digital finance, while the rest of tokenized assets remains much smaller, but strategically important.

Chart: Stablecoins are many times larger than the rest of on-chain tokenized assets, showing that digital money has already reached infrastructure scale, while tokenization of other asset classes is only beginning its institutional expansion.

This visual comparison matters because it removes a common misunderstanding from public discussion. When tokenization is discussed, it often creates the impression that the entire on-chain financial economy is already massive. In reality, most of that scale currently comes from stablecoins. Other classes of tokenized assets are still nowhere near that level.

That does not reduce their importance. On the contrary, it shows the natural order of development. First comes digital liquidity. Then comes digitization of the instruments that can use that liquidity. If that process continues to expand, tokenization will not remain an isolated sector of crypto, but a layer through which certain parts of the financial system operate.

4. Structural implications

For companies, the most important implication is operational efficiency. Stablecoins and tokenized instruments create room for faster settlement, programmable payments, more efficient collateral, and easier cross-border capital flows. That does not mean all traditional systems will disappear, but it does mean pressure on them is increasing.

For investors, the biggest shift is not simply a new asset class, but a new form of access to existing assets. Tokenization can potentially enable fractionalization, easier access, broader liquidity, and technically simpler inclusion of global participants in markets that were previously more closed or more expensive to distribute.

For banks, the implications are more complex. This is exactly where the ECB has raised concerns: if stablecoins become a widely accepted instrument for storing and transferring value, part of the funds could move out of traditional bank deposits. That increases banks’ reliance on more expensive funding sources and could weaken monetary policy transmission. In other words, stablecoins are not just a technological innovation; they can also become a macroeconomic factor.

For regulators, 2026 brings an interesting contrast. The European tone is more cautious and focused on systemic consequences. The American tone is currently more pragmatic and technology-neutral. Joint US banking guidance from March 5, 2026, made it clear that tokenized securities do not require additional capital treatment simply because they use blockchain. That is an important signal for institutional participants: the technology itself no longer has to automatically imply a regulatory penalty.

This divergence in approach could become one of the main factors shaping the geography of market development. Innovation tends to accelerate where there is enough regulatory clarity for major players to build products without fearing that the core rules will be suddenly redefined.

5. Forward look

Over the next one to three years, the most realistic scenario is not a complete transformation of the financial system, but a selective institutionalization of tokenization.

The first scenario is gradual integration. In this path, stablecoins continue to grow as a tool for moving liquidity, while tokenized treasury and fund products become a standard part of the offering of certain financial institutions. This is currently the most likely route, because it does not require a revolution — only gradual adoption where there are obvious operational advantages.

The second scenario is accelerated institutional expansion. This becomes possible if regulation in key jurisdictions matures further and large financial players begin offering more tokenized instruments with direct integration into existing platforms. In that case, tokenization could move from pilot phase to serious market expansion well before the end of the decade.

The third scenario is slowdown caused by regulatory and infrastructure friction. This could happen if authorities conclude that stablecoins pose too large a systemic risk, or if interoperability between blockchain systems and traditional financial institutions remains technically and legally underdeveloped.

The most important risks, therefore, are not exclusively market risks. They are infrastructural, regulatory, and political. The greatest opportunity is not another speculative cycle, but the possibility that certain parts of the financial system become faster, cheaper, and programmable.

If that happens, history may show that stablecoins were not just “a useful tool for crypto trading,” but the first widely adopted digital bridge between traditional money and on-chain finance.

Conclusion

Stablecoins and tokenization in 2026 are in two different stages of the same process. Stablecoins have already reached a level at which they function as digital liquidity infrastructure. Tokenization of other assets is still far smaller, but it is increasingly moving out of the experimental zone and into the institutional sphere.

That is why the real question is no longer whether blockchain can carry financial products, but which parts of the financial system will move first once operational, regulatory, and market conditions become favorable enough.

If the current trend continues, crypto in the coming years will no longer be defined only by prices and speculation, but by its ability to become the invisible infrastructure layer through which value moves more efficiently than it does today.

Note: This text is educational and informational in nature.